Beta slippage is a multi-day tracking inefficiency found in leveraged funds. Leveraged funds must rebalance over a predetermined time frame. For example a daily leveraged fund rebalances at the market close each day. This means the price movements are calculated on a percentage basis for that day and that day only. Due to rebalancing, the daily leveraged fund does not track true to its underlying index over a multi-day period. This structural tracking inefficiency caused by the leveraged funds need to rebalance is defined as beta slippage.

Example

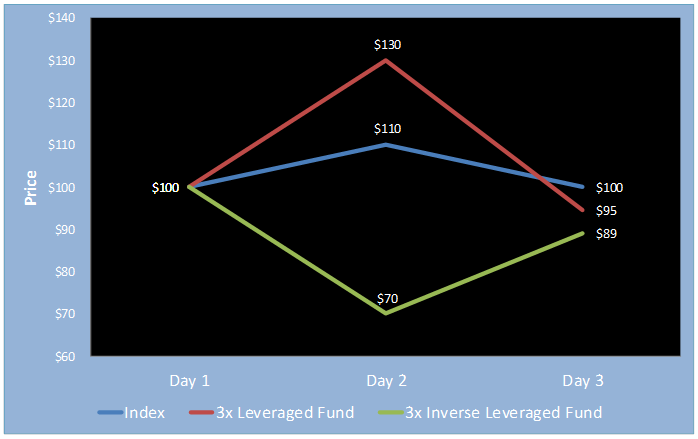

The following is a multi-day example of how beta slippage could affect a 3x daily leveraged or inverse leveraged fund.

Day one: The tracked index & 3x daily leveraged funds’ price all start at $100.

Day two: The index moves +10% and the 3x leveraged funds move +/-30%

Day three: The index moves -9% which returns it to the original value of $100. The 3x leveraged funds move +/- 27% and you would expect them to return to their original value of $100, but that is not the case! The 3x leveraged fund goes down to $95 and the inverse up to $89 for a multi-day loss of $5 and $11 respectively.

These losses are an example of beta slippage. HIT Capital has discovered how to beta slippage into gains through its proprietary trading strategy.