To our Partners,

It is amazing to think another year has already gone by. I’ll take a moment to recap 2019 before blasting into some of my thoughts for 2020 and beyond.

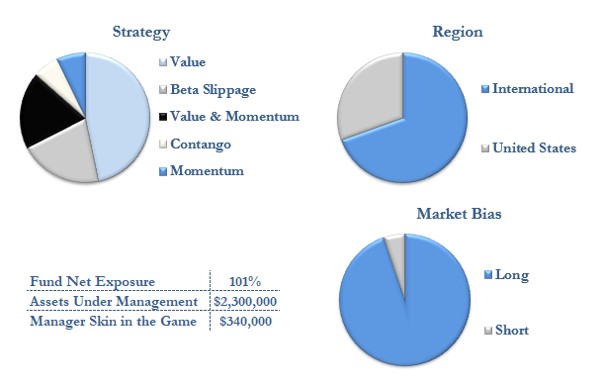

2019 was a productive year for HIT as global equity markets boomed and our fixed income research bore fruit. HIT Capital appreciated 28.9% giving us a 12.6% compounded annual growth rate since our inception in 2013. The index funds we benchmark against had good years as well: Vanguard Total International Stock Index, S&P 500, and the Hedge Fund Index gained 20.1%, 30.6% and 14.7% respectively. We added an international index to give one more perspective as HIT Capital’s portfolio is now 70% international.

Market State

Since 2009 the S&P 500’s price has increased twice as fast as the underlying business’s earnings. This has resulted in the S&P 500 becoming historically and globally expensive. While in 2018 the market tried to correct itself with a drawdown, and Trump’s tax reform strengthened earnings, it was not enough to buck the trend through 2019. America remains expensive.

The US national debt reached $23 trillion** in 2019 and it continues to grow and compound in the wrong direction.

Markets are cyclical and will go through natural periods of expansion and contraction. However, the current high domestic valuations coupled with large (and growing) domestic debt are harbingers for a significant drawdown. Of course, I don’t know, nor can anyone tell us when that will happen, but the data can show statistically it is more likely to occur.

Everyone mostly agrees that rising debt increases risk. We at HIT also believe that high valuations add to this risk, particularly when valuations exceed earnings like they do today. Wellershoff & Partners released a study a few years ago that confirmed our theory. They studied multiple markets, some of which went back 100 years, and found a striking correlation between valuation (CAPE) and drawdowns. As valuation increased so did the average drawdown over the ensuing 5 years. When Mr. Market paid $10 for a $1 of profit the average drawdown was 10% but when paying +$30 for $1 of profit (as the USA is now) the ensuing 5-year average drawdown was 35-45%.

What we are seeing in our disproportionately high domestic valuations is the primary reason why HIT Capital shifted from a majority investment in Contango and Beta Slippage which do well in flat and up markets to the Value strategy found in cheaper international markets.

Cognitive and Behavioral Bias

Humans suffer from a home bias and are led to believe everything is better were they live. This is a somewhat well-known cognitive bias in the behavioral economics community but not as well known throughout the investor community. The data shows US savers invest on average 66% of their assets domestically***. This bias is not limited to Americans, as the Japanese invest more in Japan, Canadians invest more in Canada and so on.

If you have home bias and live in the USA, there has been no better time to adjust your allocation. The USA has become one of, if not the most expensive market in the world. Nine separate value indicators show the USA to be in the top 5 most expensive markets with Price to Book having the USA as the most expensive.

You may think the USA is the greatest nation in the world and has always commanded a price premium but that has not been the case. Over the past 10 years, since the financial crisis, the USA has been steadily outpacing the globe in price.

Allocations

We cannot predict the future nor be ready for all black swan events, but we can make small bets where the historical and theoretical odds are on our side. We acknowledge the domestic and largest market in the world is expensive. But because of our inability to predict the future and the exact timing of the next drawdown we continue to bet on human ingenuity and global growth. HIT Capital is fully vested and continues to allocate across our strategies of Beta Slippage, Contango, Value, and Momentum. Under the current market conditions, our largest bet is on Value as it accounts for 66% of our portfolio.

Research

Due to Value being the strongest in international markets, we are beginning to focus our research there. HIT Capital is relatively small, so we have an inherent advantage over the institutions. Over the coming years we will be looking to expand our universe to include the foreign, small, and less-liquid stocks not available in the standard big box funds.

On a different note, Schwab entered into an agreement to acquire TD Ameritrade in November and the transaction is expected to close the second half of 2020. This could directly affect HIT Capital as TD Ameritrade is our broker and has an advantageous fee structure (there are none) when trading Contango and Beta Slippage strategies. The merger could expand the access of Beta Slippage internationally (would be great), or the more likely scenario is Schwab adopts a new fee schedule. In either case we will follow the transaction, adjust accordingly, and communicate the results in a future update.

Tax and Audit

Our annual independent audit is underway and in the upcoming weeks/months our auditor, Berkower, will be reaching out to confirm your contributions, distributions or inactivity. These confirmations are typically on the critical path and your feedback is appreciated by our tax experts working on the fund’s K1s.

For those of us invested in HIT Capital through taxable accounts, this will be the first year we see a material capital gains tax passed through due to transitioning out of an expiring Contango position that had done extremely well.

Regulatory Updates

We are currently undergoing our 3rd surprise audit and 1st by the Texas State Securities Board. The TSSB has been very thorough and has requested to review all our documents versus the more common spot check previously done by the New Mexico Securities Division. Once completed I am looking forward to reviewing the results which will be available to you as well upon request.

If you are interested in reviewing our privacy policy or my ADV, the link to each is below. (Both are required to be distributed to you annually).

Conclusion

2019 was a strong year and we continue to see a bright future, but not without the expected and unexpected bumps.

We look forward to experiencing the journey alongside you for years to come. Until next time have a safe, prosperous and joy filled 2020.

Warm Regards,

Stephen Read

References:

*https://www.thebalance.com/current-u-s-federal-budget-deficit-3305783

**US Treasury

***International Monetary Fund

WhiteHouse.gov. “A Budget for a Better America, Fiscal Year 2020,” Accessed Nov. 20, 2019.