To our Partners of HIT Capital,

2020 was an exciting year and although the first quarter started off in the wrong direction, our investments finished strong. The latter half of the year was not only good for performance but years of research and hard work came to fruition with our database of stock financials coming together.

I have a lot to be thankful for and I am realistically optimistic for HIT Capital going forward. Below are a few of our performance and research highlights:

-

2020’s performance returned 17.88%

-

We broke two monthly performance records. In April we gained 14% and then 20% in November.

-

In August we had our first working fundamental stock database

-

In October we sourced our first investment from the database

-

In December our first investment derived from the database had doubled in value

-

We did not suffer from Loss Aversion (more below)

Performance

HIT Capital finished 2020 up 17.88%, which was above our global benchmarks: International 8.62%, S&P 500 16.16% and the hedge fund index 11.11%. This brings HIT Capital’s compounded annual growth rate to 13.2% and total return since inception to 169%.

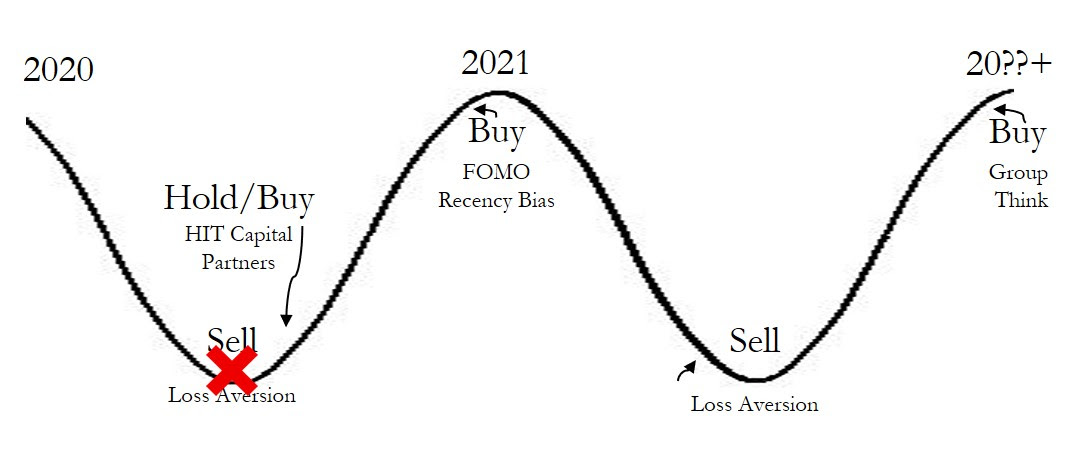

Unconscious, Cognitive, and Behavioral Biases – Loss Aversion

The beginning of 2020 forced us to feel our aversion to loss when the markets around the world plummeted. Our natural behavior is to respond more powerfully to threats than to opportunities. Financially speaking, loss aversion, may help us shy away from potentially ruinous investments but on the flip side it can team up with other biases (group think, recency bias and fear of missing out) to push us to sell low and buy high.

In the first quarter HIT Capital lost 38% of its value and this should have triggered a stronger response than the enjoyment of subsequent and equivalent gains. Personal experience, psychological tests, and the top behavioral economists agree that our human response is to pull out and protect our money, but in this instance we did not succumb to our behavioral biases. As a partnership we held tight and some even took the opportunity to go against the grain and invest more.

This could not have been easy and is a testament to each of you and your fortitude, experience, and trust to go against natural instinct and bias.

You are a special group of partners who exhibit the behaviors I try to portray in HIT Capital, the greater HIT Investment community, and ultimately pass down to my own children. 2020 was a tough year for many of us and your ability to overcome loss aversion bias did not go unnoticed. Thank you.

Research

Our research focused on building a financial database to assist in picking value and momentum stocks from a grander universe. With the help of Financial Modeling Prep, Chuck Severance (PY4E) and multiple Pythonistic colleagues we reached our milestone and completed a working fundamental stock database. Since August, when the database was completed I have continued to tidy and clean 9,288 companies financial data while simultaneously creating quantitative value and momentum screeners. I plan to continue cleaning, tidying, and improving our screens as investments sourced from our database become a larger slice of HIT Capital’s portfolio in the years to come.

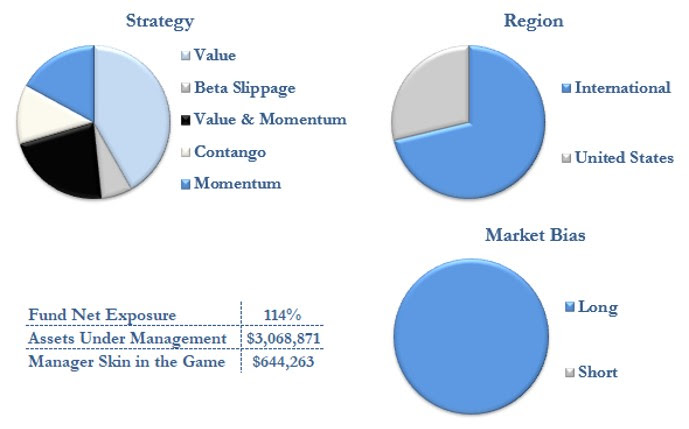

Strategies of Value, Momentum, Beta Slippage and Contango

We have opportunistically added to our Contango, Value, and Momentum strategies while reducing our Beta Slippage position. The market volatility increased our Contango strategy’s upside while reducing its downside and the completion of our fundamental stock database strengthened our Value and Momentum strategies.

Beta Slippage has been the workhorse of HIT Capital since we started trading in 2013, so why am I reducing its position now? The Strategy is still solid but it is only available with-in the S&P 500 and Nasdaq 100 universe. The S&P 500 and Nasdaq 100 encompass more than 80% of the USA’s market capitalization and I have low expectations for the overall US market. When I rank markets with quantitative value and momentum metrics, the USA now comes up as the worst market. This is the reason our Beta Slippage position has been and may continue to be reduced. For more on USA valuations and risk see last year‘s report here.

Allocations

Value is our strongest position (42%) followed by Value & Momentum (22%), Momentum (17%), Contango (12%), and Beta Slippage (7%). At the end of March, we fully exited our only market short position and currently hold only long positions. If the United States prices continue to grow at a pace greater than underlying earnings we may consider using Beta Slippage as a hedge against a stock market decline through a USA market short position.

Regulatory

HIT Investments and HIT Capital are both still undergoing an audit by the Texas State Securities Board. I suspect the Coronavirus is still playing a role as we have not received an initial audit response from their surprise visit in late 2019.

If you are interested in reviewing our privacy policy or my ADV, the link to each is below. (Both are required to be distributed to you annually).

Conclusion

Thank you for investing alongside me and for your fortitude to resist loss aversion bias. I have high hopes for the years ahead with our new financial database accompanying our proven strategies. I hope your families continue to stay healthy and happy. Until next time have a safe, prosperous and joy filled 2021.

Warm Regards,

Stephen Read