To our Partners,

HIT Capital’s loss in 2018 was 18% in comparison to the S&P 500 Total Return and Hedge Fund Index’s loss of 4% and 5% respectively. This gives HIT Capital an 11% compounded annual growth rate and an outperformance of the Hedge Fund Index by 51% and an underperformance of the S&P 500 Total Return Index of 15%.

2018 Recap

It was overall a year of underperformance. Global equities lagged as did three of the Fund’s strategies: Momentum, Contango, and Value. The Beta Slippage strategy was generally neutral. The international investments were hit hard by the global market decline throughout the year and our domestic investments joined them in the fourth quarter downturn.

Conviction

Value and momentum have outperformed over the long-run but are not without extended bouts of underperformance. Value and momentum underperformed continuously for 17- and 12-year periods respectively back when the USA was emerging from the great depression of 1929.1 Thus our recent experience is a drop in the bucket when put in perspective with our long-term views.

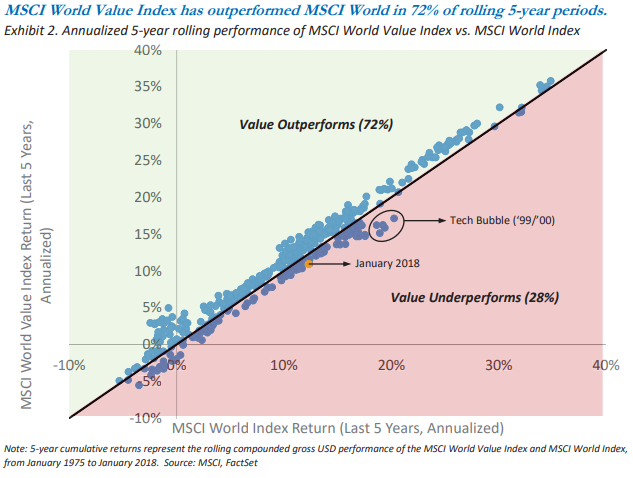

Causeway’s comparison of growth and value from 1975 to 2018 found value outperformed 72% of the time over 5-year rolling periods3.

To compound upon Causeway’s report and value/momentum research already published we backtested 265 factors of our own. The backtest was performed over 3 decades of data and the results confirmed our conviction on the strength of momentum and especially value over the long-term.

Our other two strategies, Beta Slippage and Contango do not have a long history to study but are a bit easier to predict. We continue to expect them to underperform in down years and outperform in up and neutral years, just as they have done.

Behavioral Economics

In the fourth quarter we saw our largest quarterly drawdown since inception and the S&P 500 experienced its 5th largest since 1926.2 The headlines shouted “Stock Market Crash is Coming” and I personally could feel the butterflies enter my stomach as our asset values decreased.

Being aware of my behavioral biases and the tensions felt in my gut when the markets roiled was a good reminder of why momentum and value have continued to work over the past century and should continue to work into the future.

The first bias I typically feel during a market downturn is loss aversion, the act of feeling losses more intensely than similar gains. Compounding upon the loss aversion bias, media outlets begin to hop on board (fear sells), and the headlines read like the above “Stock Market Crash is Coming.” Once the train really starts rolling in a downturn, additional biases pile on such as herding, availability, and confirmation bias. All these natural instincts lead to the temptation to be irrational in our thinking and trading, and if left unchecked, we could act upon our emotions and start selling out.

But, as long-term investors and having an awareness of our faults HIT Capital can overcome these emotions and celebrate the downturn for what it is, a sale. It may not be pre-planned like Black Friday or Cyber Monday, but the effect is similar; our future stock purchases are buying more earnings for less cost.

Outlook

Going forward our global long-term return expectation increased by about 15%. 2018 is the first year since HIT Capital’s inception the domestic and international market prices have both decreased more than 10% compared to their underlying earnings. We celebrate paying less for more and would be happy to see the domestic market prices continue to cool.

Allocations

Research

While the markets continue to do their day to day thing, we concentrate our efforts around the search for long-term risk adjusted returns. In 2018 we studied the historical performance of 265 equity factors and 16 fixed income classes across the globe. Some of the highlights we drew from the studies were:

- Equity

- Stock/business size alone does not provide a clear signal. A stock categorized as “small-cap” did not perform better than its brethren categorized as “large-cap”

- The S&P 500 was the most efficiently priced market in the world. When factors provided outperformance, the spread between the best and worst was typically the smallest within the S&P 500 as compared to the Russell 2000, international and emerging markets.

- Volatility and analyst expectation factors did not provide a strong positive or negative signal.

- Value factors gave the strongest signal in both spread (difference between the top and bottom quintiles) and absolute returns.

- Value factors were enhanced within smaller stocks.

- Value factors worked globally.

- Fixed Income

- Peer to Peer marketplaces appear to be returning more risk adjusted return than traditional fixed income classes.

- Private real estate loans appear to be mispriced. They were earning the highest fixed income risk adjusted return by a margin of 1-5% per year.

- International bond yields are dismal and not expected to compete with inflation.

We will continue to build on our research and focus on optimizing our value strategy and taking advantage of the peer to peer marketplace in the near term.

If you are interested in purchasing HIT Capital while it’s on sale or adding private real estate loans to your portfolio, please send me a note.

Thank you for a productive 2018. God bless, and we wish you a happy, healthy and prosperous 2019.

Warm Regards,

Stephen Read

References:

1 https://www.morningstar.com/blog/2018/09/13/factor-based.html

2 https://awealthofcommonsense.com/2018/12/buying-when-stocks-are-down-big/

3 https://www.causewaycap.com/wp-content/uploads/2018/02/201802-TheCompellingCaseforValue-1.pdf

Additional Information:

The annual ADV update and privacy policy notification is still mandated to share annually and can be found through the following two links.

Maria Hall has begun our annual fund audit and will be contacting you to confirm contributions/distributions. Once the audit is complete your personalized K1’s will follow.