To our Partners,

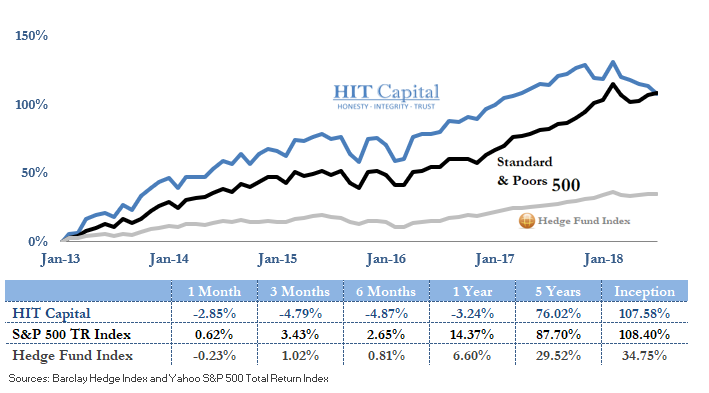

HIT Capital’s loss in 2018 was -4.87% in comparison to the S&P 500’s gain of 2.65% and Hedge Fund Index’s 0.81%. This gives HIT Capital a 14% compounded annual growth rate and a similar performance to the S&P 500 Total Return Index and an outperformance of the Hedge Fund Index by 73%.

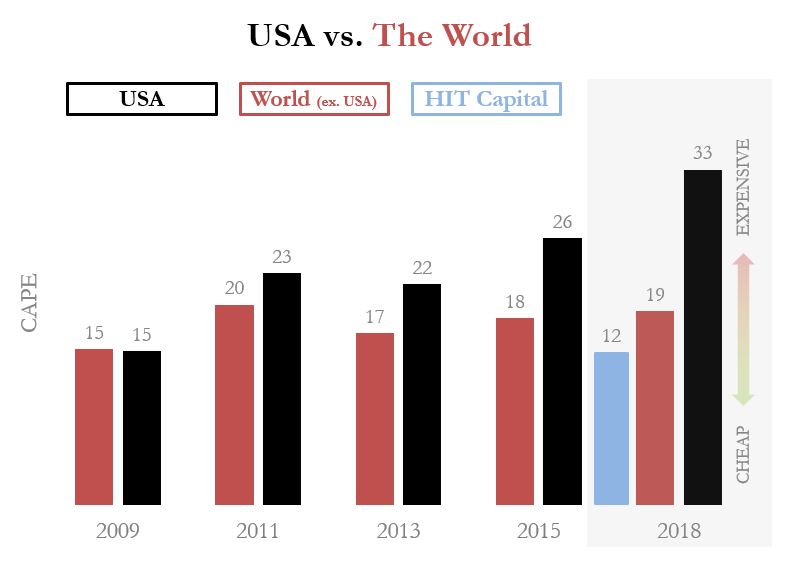

We can’t beat the market all the time, but we can continue to invest in strategies based on long term empirical evidence, not short term price movements. Historically cheaper markets have performed better than expensive ones, but in the short term cheaper markets can always get cheaper, as we saw with our foreign investments in the first half of 2018.

It feels like only yesterday we were in the weeds scouring for an edge while my colleagues in business school were studying the efficient market hypothesis. While they learned it was impossible to beat the markets we discovered what we thought to be the biggest mistake since the Austrians fought themselves in the battle of Karansabes.

Wall Street had just launched a new financial product that would allow the masses to double or triple their market exposure. On the shell it sounded wonderful, who wouldn’t want their money to grow at 300% the normal rate.

The problem was, as a few investors learned, the products suffer from a little-known re-balancing flaw we initially coined Volatility Drag and the broader market later defined as Beta Slippage.

Since the market lets us bet for or against investments, instead of betting for the Austrians we bet against them. Beta Slippage may not have been as big of a mistake as the Austrians accidentally fighting themselves, but it did result in the birth of HIT Capital and much of the fund’s out-performance.

Since the birth of Beta Slippage in 2009 we have grown from an idea to a multi-strategy, multi-million-dollar fund that has more than doubled in performance since inception. It has been a rewarding journey thus far and we look forward to sharing the next 5 years with you as we did the last.

Investing is as much learning from the past as it is being in the present and looking to the future. Since the birth of Beta Slippage, the US market has been on a tear, taking us from an averagely priced market to one of the most expensive in the world. HIT Capital began investing in 2013 and we have been a large beneficiary of this domestic market tear but as the markets change so does our portfolio.

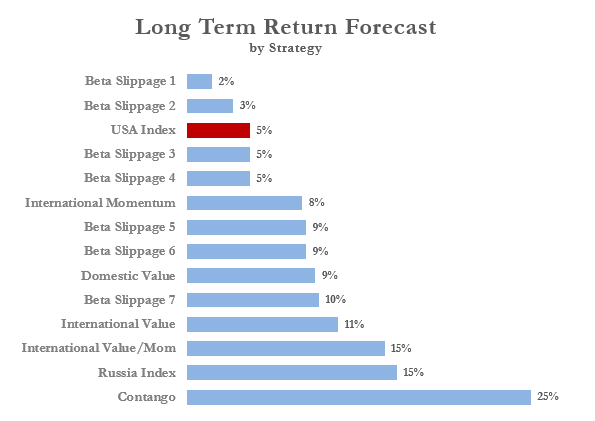

In our process to construct the optimal portfolio we combine our long-term market return forecasts with each strategy’s estimated outperformance.

All things being equal, our portfolio would match proportionately with the estimated returns. Higher returns equal more allocation and vice versa. Unfortunately, the strategies and underlying market assumptions are not equal. Cost, liquidity and drawdown risk are all interrelated with returns and are considered when creating HIT Capital’s portfolio. Our optimal portfolio is not so much constructed by a complicated equation based on volatility and co-variances, like this one found in a portfolio theory class:

All things being equal, our portfolio would match proportionately with the estimated returns. Higher returns equal more allocation and vice versa. Unfortunately, the strategies and underlying market assumptions are not equal. Cost, liquidity and drawdown risk are all interrelated with returns and are considered when creating HIT Capital’s portfolio. Our optimal portfolio is not so much constructed by a complicated equation based on volatility and co-variances, like this one found in a portfolio theory class:

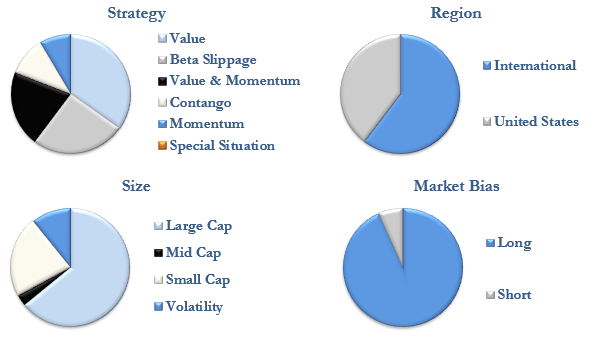

The interrelations of the investments are important from a macro sense as we want to diversify across markets and strategies with a goal of decreasing the odds of extreme drawdowns. The interrelations associated with volatility and co-variance during rational market periods are not.

Any of our investments could go to zero, at any time, for a multitude of reasons just as all investments can. A recent example is one of our Contango investments. The Contango strategy has historically been the fund’s best performing strategy returning more than 50% a year, and we believe it to have potential for strong returns going forward (See return chart above).

In combination with these strong returns is the potential for large drawdowns. This past February we saw one of our contango investments move over 100% in the wrong direction, but because of our risk adjustment and how it melds into the fund’s overall portfolio, HIT Capital lost about 5% over that same period.

Thus, when we choose our allocation weightings, we prioritize returns alongside drawdown risk.

HIT Capital’s past 6-month returns may not show it but we are enthusiastic at the opportunities being found abroad. In order to fully capitalize on these opportunities, we are in the midst of studying over 250 fundamental factors across the globe and we look forward to sharing a few of the findings in our end-of-year update.

Until then, thank you for being part of our HIT family and we wish you a happy, healthy and prosperous future.

Warm Regards,

Stephen Read